The Arabian Peninsula, a growing area

A crossroads for trade between Southeast Asia, North Africa, and Mediterranean Europe, the Gulf countries are characterized by remarkable economic dynamism, which is also a consequence of diversification policies in the non-oil sector. The strong commercial ties with Italy

The Gulf countries, as is well known, are also the focus of public initiatives to support our operators abroad, at a time when the trade war is forcing them to diversify their markets and find alternative trade routes. The Gulf countries refer to the six states - Saudi Arabia, Bahrain, the United Arab Emirates, Kuwait, Oman, and Qatar - that are members of the Gulf Cooperation Council (GCC). Among these, the United Arab Emirates (UAE) and Saudi Arabia are specifically identified as high-potential non-EU markets in the Export Action Plan presented by the MAECI last April. These two countries are therefore among the priorities of SACE – our public Export Credit Agency – towards the so-called GATE (Growing, Ambitious, Transforming, Entrepreneurial) countries, which SACE oversees with its own offices on site to promote the growth of Made in Italy.

Indeed, among the six Gulf markets, the United Arab Emirates and Saudi Arabia are traditionally our main customers in the region. According to SACE's Export Action Plan, the former is the 16th largest destination market for Italian exports and the 1st largest market in the MENA (Middle East and North Africa) area. At the same time, Saudi Arabia is the 19th largest destination market for Italian exports and the 2nd largest in the MENA area. In support of the increased interest in these trade routes, it can be seen that in the first half of 2025 alone, several initiatives in Italy promoted high-level trade relations with these markets. Among the many, we mention the Italy-UAE Business Forum and the Arab Italian Business Forum (AIBF25).

During the Italian government's mission to Saudi Arabia at the beginning of the year, SACE signed agreements with leading Saudi counterparts worth a total of $6.6 billion, with the aim of supporting Italian exports and trade and investment relations between the two countries. In this context, a memorandum of understanding was also signed with the local sovereign wealth fund, the Public Investment Fund, worth USD 3 billion, to promote the involvement of Italian companies in Saudi Arabia. The agreement aims to facilitate companies in the projects envisaged by 'Saudi Vision 2030'.

A hub that consolidates its role as a strategic junction towards Asia and Africa. In the new global trade scenario, which has been taking shape since the beginning of 2025, the Gulf countries are increasing their strategic role in intercepting and brokering business with Asian and African trade routes. This is evidenced by the increasing frequency with which managers and commercial offices operating in the Emirates, for example, refer to their area of expertise as MEASA, which defines an area comprising the Middle East, Africa, and South Asia. Another significant new development is that, while the UAE has traditionally been the region's leading trader, Saudi Arabia is now emerging strongly in this role. The challenge posed by Saudi Arabia to Dubai and the Emirates in this game stems from several factors: favorable logistics (a dozen ports located not only on the Persian Gulf but also on the Red Sea), a strong push for non-oil diversification of the economy, a rapidly growing population (Saudi Vision 2030 estimates an increase to 50 million from the current 35 million) and an increasingly large youth component. To achieve these objectives, Saudi Arabia is also following the UAE model by developing districts geared towards foreign investors, in which the partner can only be foreign, with customs facilities and favorable taxation. The Saudi formula is that of SEZ, special economic zones.

In the UAE - the first to launch this instrument - there are over 40 Free Trade Zones, some of which are specialized and others multi-sector. Among the former, we highlight: DIFC (Dubai International Financial Centre) in the financial services sector, Dubai Multi Commodities Centre (DMCC) for commodity trading (from oil to wheat), and Dubai Media City (DMC). Several others are more oriented towards commercial, industrial, and logistics activities, and the best known, perhaps also due to its decades-long history, is the Jebel Ali Free Zone Authority (JAFZA), whose construction began in 1979 in parallel with the first regulations governing this new reality. JAFZA has a wide range of specializations: agriculture, aviation, commodities, energy, food & beverages, healthcare and pharmaceuticals, industry, logistics, mechanics, packaging, and trade.

FTZs are characterized by efficient infrastructure, dedicated services, and extremely favorable corporate conditions: 100% foreign capital is allowed, profits can be repatriated, and there are corporate tax and customs exemptions (corporate tax and customs duties). However, it should be noted that the Emirates that make up the UAE compete with each other – particularly with Dubai – to attract foreign investment. We therefore suggest that information be sought more effectively on individual Emirates, for example, to obtain more data on the free zones of RAKFZ Ras Al Khaimah or Fujairah Free Zone FFZ.

In Saudi Arabia, on the other hand, the Special Economic Zones are more recent and based on the Vision 2030 plans. The five current SEZs aim to expand business opportunities in the Kingdom of Saudi Arabia by attracting high-quality investors, technology transfers, diversifying the local economy, and strengthening strategic sectors. Other Gulf countries - Qatar, Oman, Kuwait, and Bahrain - are also developing similar initiatives and offer support in identifying the most suitable structure for foreign companies' business projects.

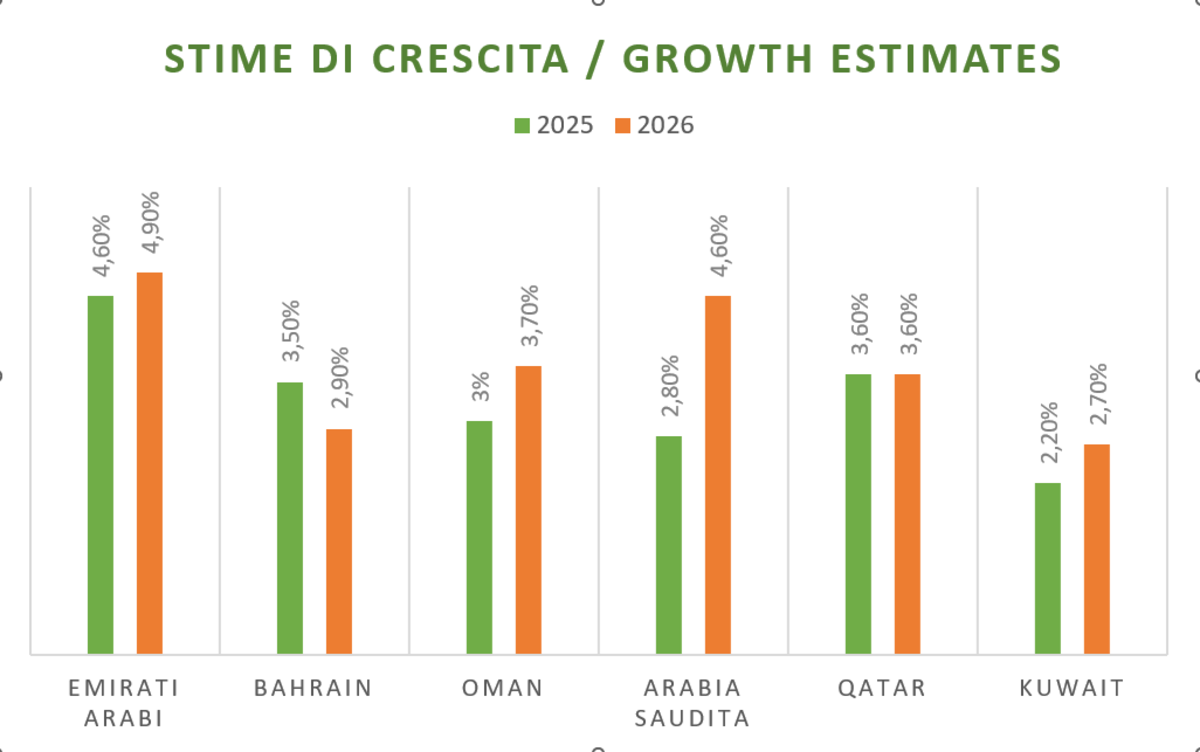

Growth prospects for the economy and GCC countries. The latest data from authoritative international sources on the economic prospects of these countries are those of the World Bank for June 2025. Economic growth of 3.2% is forecast for the six countries as a whole in 2025, and the estimate for 2026 is 4.5% (compared to a modest 1.7% in 2024). However, given the instability of international trade and the risk of recession for some of the major players in global trade, the Gulf countries are further pushing for economic diversification and the strengthening of regional trade, as recently pointed out by Safaa El Tayeb El-Kogali, World Bank's Country Director for (GCC) countries.

Moving on to individual countries, the most significant growth estimates are forecast for the United Arab Emirates (+4.6% in 2025 and +4.9% in 2026), thanks to public investment in improving governance and the expected expansion of partnerships with foreign countries. For Bahrain, estimates for 2025 are +3.5% (+2.9% in 2026), supported by the country's Economic Vision 2030 program, which focuses on infrastructure, logistics, financial technology, and tourism. Growth in Oman is expected to accelerate gradually: 3% in 2025, 3.7% in 2026, and 4% in 2027, driven by robust performance in construction, manufacturing, and services. Given the size of its economy, the figures for Saudi Arabia are incredibly significant. World Bank estimates project a recovery to 2.8% in 2025 and an average of 4.6% for 2026-2027. If we exclude oil-related growth, growth in the non-oil sector for the three-year period 2025-2027 is projected to average 3.6%, with the Kingdom of Saudi Arabia committed to pursuing the economic diversification set out in its Vision 2030 agenda. In Qatar, the national product is expected to increase by 2.4% in 2025 (2.6% in 2024), with a subsequent acceleration of 6.5% in the two-year period 2026-2027, driven by the hydrocarbons sector. In Kuwait, a robust economic recovery is expected (+2.2% in 2025), following declines of 2.9% (2024) and 3.6% (2023). The boost in the non-oil sector will come from major infrastructure projects. In the 2026-2027 period, economic growth is expected to be around 2.7%.

{kind=link}

{kind=link}

{kind=link}