Mechanization in Australia, an expanding sector

The twelfth world economy continues to grow, and it also does so in the name of agriculture and avant-garde mechanisation. Forecasts indicate that over the next five years the sector is expected to grow by 7.3% per year to reach a value of 4.5 billion Australian dollars

Getting lost in Australia gives you a lovely feeling of security.” The greatest traveller of the 20th century, Bruce Chatwin, spoke of a country that is worth a continent with its 7.6 million square kilometres (about 26 times the size of Italy) but which is home to just over 26 million inhabitants, definitely less than half of the Italian population. A remote, complex place with an aggressive nature but also in development and strongly open to the world market. It is no coincidence that Australia is the twelfth economy on the planet with a GDP of 1,600 billion dollars and with a growth that the International Monetary Fund has set at 1.6% in 2023 and estimates at 1.7% in 2024. Not the Indian and Chinese levels, but still values more than double those estimated in the Old Continent. The macroeconomic picture is generally stable: rising inflation, increases in means of production and increases in labour costs are worrying, but the faces of economic operators, including agricultural entrepreneurs, are marked by smiles. Thanks also to the strong predisposition to exports and to an Australian dollar that has long forgotten its volatile phases and remains a lever for the competitiveness of companies in the markets.

Australia, a hyper-extensive agriculture. In this scenario, the role of agriculture remains important. Some numbers, taken from the Australian Agricultural Machinery Market Report 2023, produced by FederUnacoma in collaboration with KG2 and the ICE Agency, provide a detailed picture of the Canberra universe. Australian agriculture in 2023 was worth about 92 billion Australian dollars (at the current exchange rate approximately 60 billion euros) made by just under 90,000 farms on 360 million hectares. And here a 'hors categories' figure emerges: the average area is more than 4 thousand hectares. The agricultural sector represents 11.6% of exports of goods and services, 2.4% of GDP and employs 2.5% of the labour force. Excluding forest production, agricultural activities occupy 55% of Australia's surface. Already from these numbers, the hyper-extensive characteristic of the sector is evident. Largely committed to satisfying the food needs of more than 24 million head of cattle to which 68 million sheep are added. And so we are faced with almost 25 million hectares of arable land, with the lion's share of 13 million hectares of wheat and 5 million hectares of barley, with an outline of more than 3 million hectares of rapeseed and almost 1.2 million hectares of hay and silage. The imprinting remains evident. But it should be noted the tendency to change in the weight of the various sectors: vegetable products, oilseeds and legumes are growing, traditional sectors such as those of wool and milk are retreating.

Increasingly large companies. This evolution has also affected farms, whose number has fallen sharply in recent decades in parallel with the progressive increase in average size. The losers have been the small farmers, unable to bear the effects of a climate change that in Australia seems to have played in advance. Extreme temperatures and minimal winter rainfall have put a strain on agricultural performance, so much so that the Report, while also mentioning the significant increase in production costs, highlights a 23% contraction in agricultural profits in the period 2001-2020. Decrease that resulted in the expansion of the areas and the volume of business of individual agricultural enterprises: the large size has become the first and probably the only answer to the reduction of margins. Moreover, after two record years in which the above-mentioned share of 92 billion Australian dollars was reached, 2023, characterised by a chronic and invasive drought, registered a 14% contraction, stopping the added value at around 80 billion dollars and significantly moving away from the government's stated objective: 100 billion dollars by 2030.

A complex situation. And so, in the face of long-term fundamentals all in positive ground, the short-term economic situation relative to the 2023-2024 forecasts sees a sequence of minus signs, often in double digits. Wheat production is expected to fall by 36% to 25.4 million tons, 4% lower than the 10-year average. This decline was not compensated by prices, which fell by 7%. Barley is on the same wavelength, with production down 26% to 10.5 million tons and prices down 10%. Even more evident is the contraction of rapeseed, with production down 38% to 5.2 million tons, while the production decrease is a little less marked for cotton (-8%). Conversely, some sectors continue their expansion phase. This is the case of horticulture, which, almost indifferent to the drought problem, adds one billion to the value of production and hits the new historical record of 18 billion Australian dollars. Peaceful faces also among (cane) sugar producers who, thanks to the upward consolidation of the world price, improve the added value of the sector by 300 million dollars.

State support. There are several state programs to support the agricultural sector. The most significant (660 million Australian dollars aimed at reaching 100 billion in agricultural production within six years) is Ag2030 and involves a series of initiatives to support agricultural trade and exports with an impact also on mechanisation, thanks to direct funding for the purchase of equipment and funds intended to promote access to markets. Another 150 million dollars come from the AgResults initiative, aimed primarily at small and medium-sized farmers. In addition to the introduction of better performing cultivars, AgResults supports initiatives aimed at reducing gas emissions and, above all, promotes the adoption of innovative mechanisation technologies capable of improving the efficiency and profitability of small agricultural businesses. In the 2023-2024 state budget, 1.5 billion dollars were then allocated for a series of initiatives aimed at limiting the impact of the climate on the economic system. Of these, 302 million will come to the agricultural sector for sustainable and environmentally friendly practices.

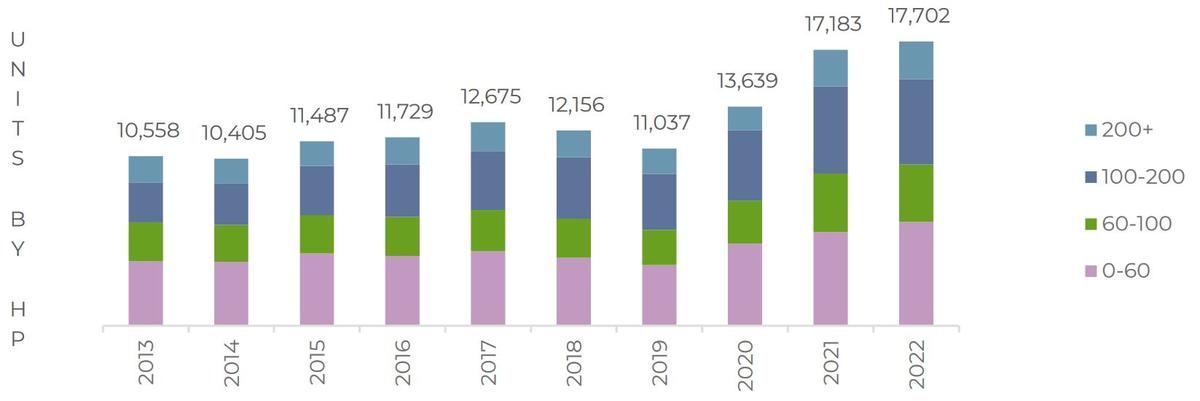

What about agricultural mechanisation? Thanks also to the Temporary Full Expensing (TFE) program, which ended in 2023, which provided significant tax incentives for the purchase of production vehicles, in 2022 the Australian tractor market reached its peak with 17,700 units sold, two billion dollars in turnover and a growth of 33% over the five-year average (just over 11 thousand tractors arrived on the market in 2019). After the peak of 2022, with all power classes growing significantly, 2023 experienced a physiological slowdown, with a more marked drop in the power class between 40 and 100 Hp (-19%).

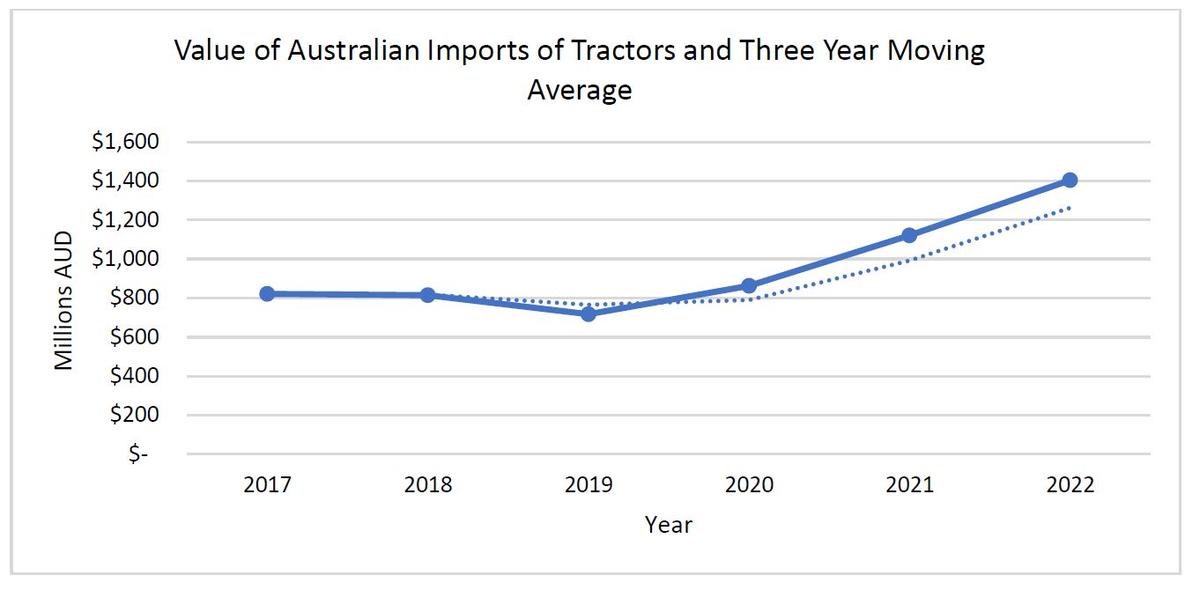

Expanding agricultural mechanisation. But, as we said, the fundamentals are good and optimism reigns in the forecasts of agricultural machinery manufacturers and operators in the sector. In fact, the sector is expected to record significant growth, from a turnover of 3.15 billion dollars (2023) to 4.48 billion dollars by 2028, with a compound annual growth rate of 7.3%. Positive prospects, which are also affected by the world's major competitors. It is not a detail that the tractor market is worth 1.4 billion dollars in imports. Segment in which the United States holds the lion's share with a market share of 33% (470 million dollars). Germany (18% share) and, at a distance, France (8%), Japan (7%), the United Kingdom (7%) and Italy (6%) follow with a value of 246 million. Moreover, Made in Italy shows a strong growth rate: in 2020 the value of Italian tractor exports to Australia was about 45 million, at the end of 2022 it was close to 80 million dollars. And there is also a ranking in which Italy is at the top: the one relating to machines and equipment for soil preparation. Australian imports from our country have almost tripled in the last three years, from 9 to 25 million Australian dollars, giving Italian manufacturers a 30% share. Almost all the medium and large global players in the agro-mechanical sector have distribution centres and branches in Australia, practically none have production plants (Mahindra has an assembly factory). Considering the lively but fragmented presence of local manufacturers, the opportunities for growth for exports to the market appear interesting. Because Australia remains far away, but it is becoming increasingly attractive.

{kind=link}

{kind=link}

{kind=link}