South America: a promising economy

Several international analysts believe that South American countries, despite their well-known structural vulnerabilities, are less influenced by the factors of economic and geopolitical instability that are affecting the Persian Gulf area, Europe, and even the USA

The opportunities created by the EU-Mercosur Agreements must first be seen in the context of the key figures of current relations. The key figures were provided at the aforementioned Italy-Latin America Economic Forum in Prato, at the initiative of the Ministry of Foreign Affairs, the Italian Trade Agency (ICE), and IILA. Italy's trade balance with Latin American countries was in the black at EUR 6.5 billion in 2025, reflecting exports of EUR 20.3 billion and imports of EUR 13.7 billion. This represents a 3.4% increase in exports compared to 2024, while imports grew by 9.6%. Italy is the region's ninth-largest supplier, with a 1.6% market share; machinery and equipment account for 32% of the value of our exports, and transportation equipment for 16%. The picture is rounded out by the stock of Italian direct investments in the Latin American region, which amounts to EUR 40 billion, distributed among 3,273 companies, with more than 300,000 total employees and a turnover of 75.4 billion. An average per enterprise that is perhaps still undersized compared to what these markets might demand.

Regarding the numbers expressed by Latin America, it is possible to refer to the most authoritative source of economic data on the continent (and not only): the World Bank Group, which on April 8th released the report “Latin America & the Caribbean Economic Update”. According to WBG analysts, Latin America and the Caribbean (LAC) is expected to see GDP growth of 2.1% this year, just below the 2.4% growth rate in 2025. The low growth rates typical of this area are largely linked to historical structural weaknesses: growth driven by private consumption rather than investment, still insignificant inflation containment, and, consequently, restrictive financial conditions.

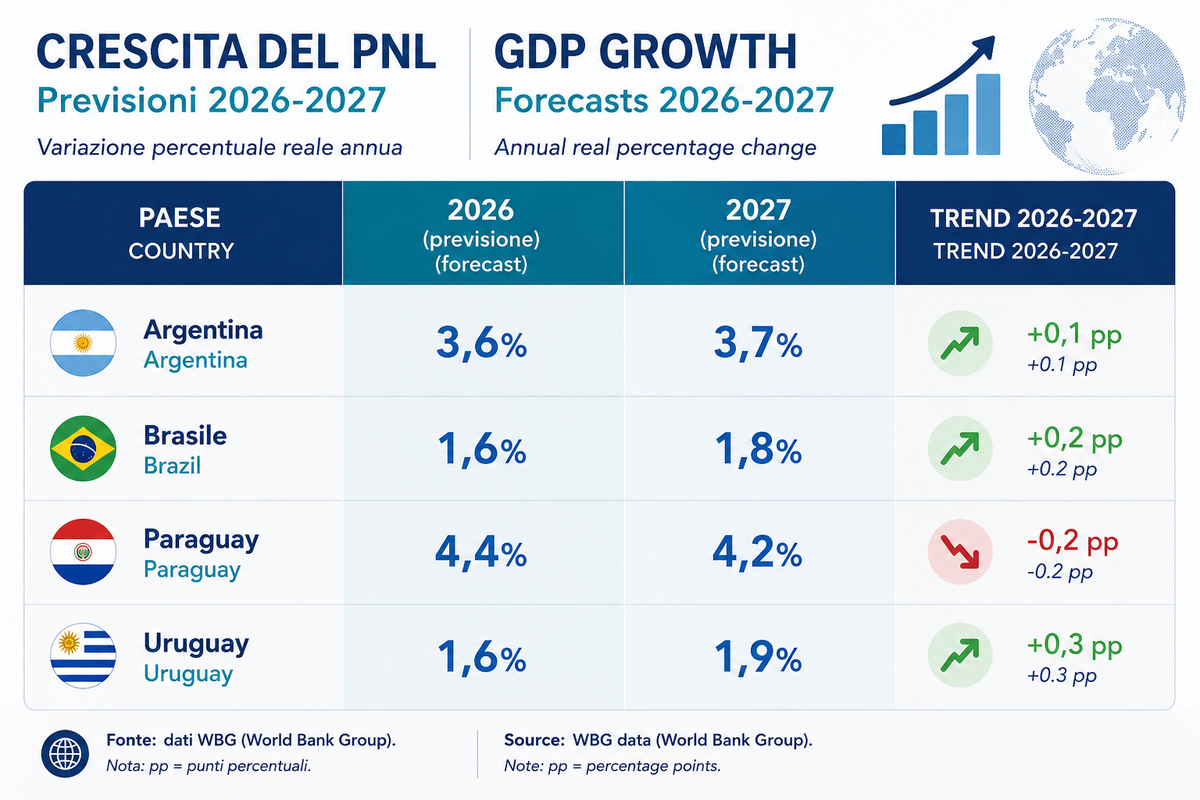

According to the WBG, from the new paradigm that is establishing itself in global trade, at least two opportunities can be seen for Latin America: a realignment with competitors as a production hub and the challenges of the energy transition that could see this region in a strategic position within new supply chains thanks to the traditional clean power mix, with respect to which the region the area appears to also be advantaged in terms of the availability of critical minerals. Foreign trade remains the key for businesses for at least three drivers: market expansion, reduction of risk concentration, increased diversification. To these ends and in light of the uncertain international trade landscape, WBG views the agreement with the EU as a factor of stability, by defining key global partners and by giving local companies the opportunity to plan the development of foreign trade relations over time. Based on WBG data for the four Mercosur countries that signed the Agreement with the EU, GDP growth is estimated to be distributed as follows in 2026 and 2027: Argentina 3.6% and 3.7%, respectively; Brazil 1.6% and 1.8%; Paraguay 4.4% and 4.2%; Uruguay 1.6% and 1.9%.

The importance of geopolitical dynamics on international trade suggests providing updated assessments of country risk, also considering the impact they have on the cost of financing and payment instruments, insurance, and logistics. In this article, it is worth mentioning the outlooks of Verisk Maplecroft and Allianz Trade, which are particularly oriented towards the corporate segment. Allianz Trade in its Outlook 2026-27 of March 31st describes a worrying scenario that estimates a global GDP growth of 2.6% in 2026 (revised downwards by -0.5 points), from which we extract the +2.1% of the USA and the +0.8% of the Eurozone. International trade growth is forecast at 1.5% in 2026 (revised downwards by -0.5 points). For completeness, inflation data is also reported: 3.2% in the United States and 3.0% in the Eurozone this year (revised upwards by 0.7 and 1.1 percentage points). In this scenario, the Report sees Latin America as “relatively more protected,” with Argentina, Brazil, and Mexico benefiting from their role as exporters of raw materials. This explains - for Allianz Trade - the regional growth estimate of 2.4% in 2026 and 2.9% in 2027, against a Eurozone of 0.8% and +1.3%, respectively.

Latin America is thus repositioning itself in a competitive scenario in which the Persian Gulf countries appear to be conditioned by geopolitical instability, which is weighing on trade, tourism and has had a negative impact on the growth forecast at the start of the year (4%), which has now been revised down to 1.9%. In Asia, growth has been effectively wiped out by the geopolitical and energy shock, while China continues to 'run' with a forecast of 4.6% in 2026. Even on the financial markets, commodity-exporting countries and emerging countries, operating on more resilient logistics routes, benefit from positive or compensatory effects: the Annual Report "Italian Maritime Economy" (SRM) mentions four of these economies, three of which are important Latin American countries: Brazil, Mexico, Colombia, and Indonesia. Verisk Maplecroft in its report of May 8th entitled Beyond the Storm: How Geopolitics Could Reshape Insurance by 2030, in light of changes in the global geopolitical scenario, assigns Latin American countries the two lowest levels of political risk – in a four-level ranking (Low Risk and Medium Risk), with the sole exception of Venezuela, Colombia and Ecuador (High Risk).

{kind=link}